What if the most significant financial hurdle to your Florida dream isn’t the down payment, but the carrying costs that reset the moment you get the keys? With insurance premiums now averaging $11,759, it’s easy to feel a sense of anxiety about the hidden costs buying a home Florida requires. We understand the frustration of navigating complex CDD fees and unpredictable property tax reassessments. You want a process that feels transparent, professional, and entirely under your control.

This guide provides the clarity you need to budget with absolute certainty for the 2026 market. We’ll break down the documentary stamp taxes, the 0.2% intangible tax, and the reality of rising HOA requirements for both condos and single-family homes. You’ll walk away with a line-item budget for your first year of ownership and the confidence to choose a representative who truly understands the local landscape. Let’s replace the guesswork with a proven, methodical path to your new home. We are here to ensure your transition is secure, stable, and predictable.

Key Takeaways

- Budget with total confidence by understanding the 2% to 5% rule for closing costs and legal transfer fees. It’s about clarity, precision, and preparedness.

- Learn why a specialized insurance strategy and a professional wind mitigation report are essential for securing the deepest premium discounts available.

- Navigate the complexities of property tax resets and CDD fees to eliminate the hidden costs buying a home Florida often presents to the uninformed buyer.

- Uncover the reality of builder fees and personalization costs in new construction to ensure your final price matches your initial expectations.

- Empower yourself with negotiation strategies that shift closing burdens back to the seller, all while leaning on the wisdom of a trusted local guide.

The Transactional Reality: Beyond the Sticker Price in 2026

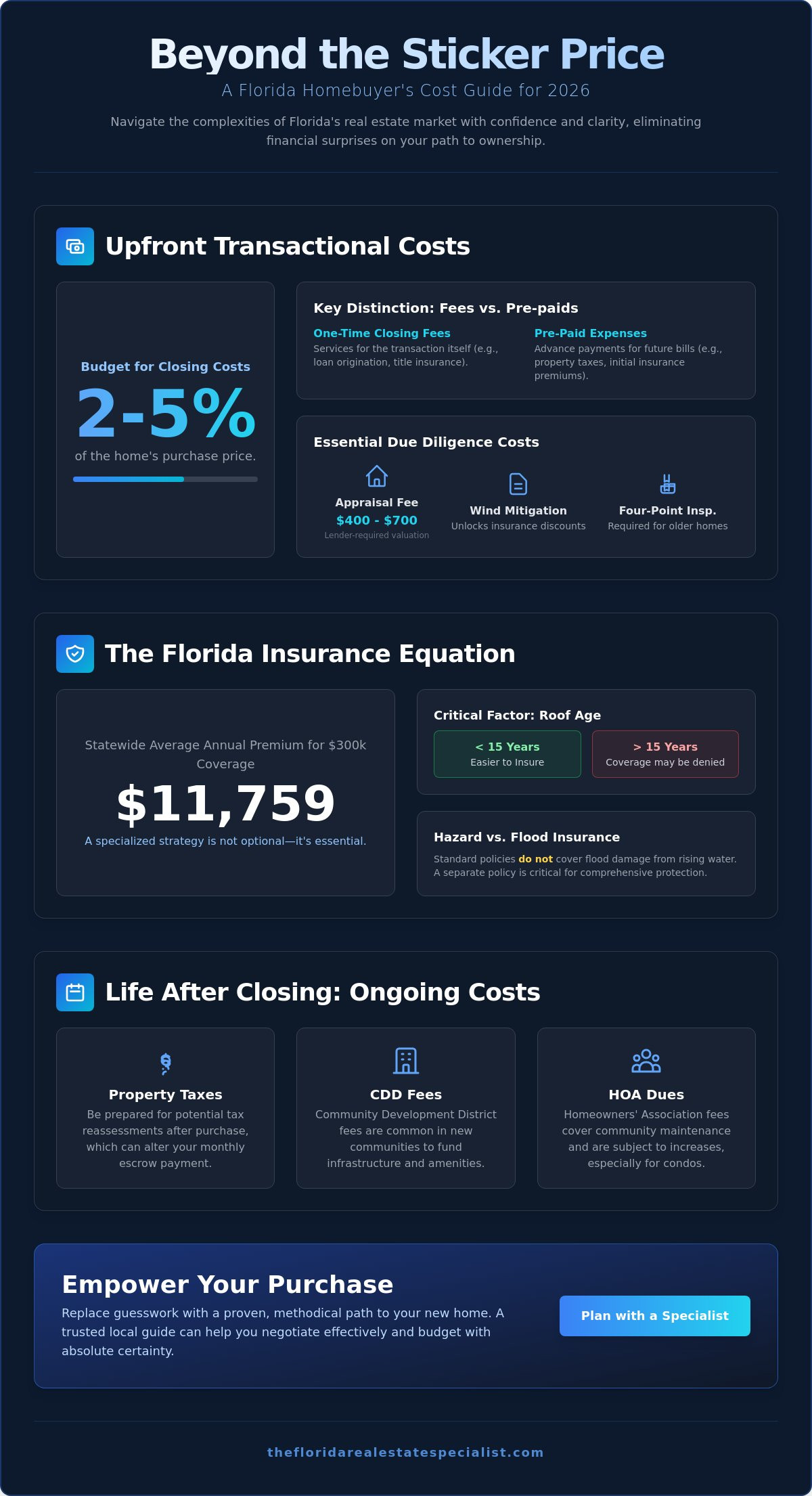

Buying a home is a milestone. It’s an achievement, a transition, and a significant financial commitment. While the sale price dominates the conversation, the transactional reality involves a series of mandatory fees required to finalize the legal transfer of property. These are often grouped together, but understanding closing costs is the first step toward a surprise-free experience. We are here to ensure that every dollar is accounted for long before you reach the closing table.

In the Florida market, a reliable rule of thumb is to budget between 2% and 5% of the purchase price for these expenses. This range covers the “big three” categories: loan origination fees, title insurance, and initial escrow deposits. However, it’s vital to distinguish between actual closing fees and “pre-paids” in your initial estimate. Closing fees are one-time costs for services rendered during the transaction. Pre-paids are advance payments for future bills like property taxes and homeowners insurance. Misidentifying these is one of the most common hidden costs buying a home Florida shoppers encounter, often leading to last-minute stress that we work hard to prevent.

The Nuance of Florida Title Insurance

Title insurance is non-negotiable for protecting your ownership rights against past liens or claims. In a high-turnover market, a clean title search ensures your investment remains secure. The cost is often split between the buyer and seller, though customs vary across the state. While certain market areas may typically see the buyer pay for the owner’s policy, other regions often have the seller cover this cost. The Florida Real Estate Specialist helps you navigate these market-specific nuances so you know exactly where you stand, replacing uncertainty with a sense of clarity and ease.

Appraisal and Inspection: The Cost of Due Diligence

Lenders require a professional appraisal to verify the home’s value, which typically costs between $400 and $700. Beyond the appraisal, specialized Florida inspections are essential. A standard inspection is just the beginning. You also need a Wind Mitigation report and a Four-Point inspection. These documents aren’t just paperwork; they are the keys to unlocking insurance discounts and identifying structural vulnerabilities. Skipping these steps in a tropical climate creates a massive financial risk. Investing in thorough due diligence now prevents the hidden costs buying a home Florida might reveal years down the road. It’s a structured path to success that protects your future and your peace of mind.

The Florida Insurance Landscape: Navigating Premiums and Protections

Insurance in Florida is not a standard checkbox on a closing statement; it is a specialized strategy that requires professional foresight. With the statewide average annual premium reaching approximately $11,759 for $300,000 in dwelling coverage, your choice of policy impacts your monthly budget more than almost any other factor. We see many buyers enter the market with a sense of anxiety about these figures. However, with the right guidance, you can find a path toward stability, security, and savings. Identifying these insurance requirements early helps you avoid the hidden costs buying a home Florida buyers often overlook during their initial search.

The age and condition of a home’s roof dictate its insurability and annual cost. Carriers now look at the age of your shingles with a level of scrutiny that can feel overwhelming without a seasoned expert by your side. If a roof is older than 15 years, many private insurers may refuse coverage or demand a full replacement before binding a policy. To mitigate these expenses, a Wind Mitigation report is essential. This inspection documents how well a home withstands high winds. It is the primary tool for unlocking significant premium discounts. Budgeting for these insurance nuances is just as vital as reviewing the official Florida Property Tax Information provided by the state to understand your total carrying costs.

Flood Insurance vs. Hazard Insurance

Standard homeowners policies do not cover damage from rising groundwater or storm surges. This is a critical distinction. Even if a property is not in a high-risk FEMA flood zone, we often recommend a separate flood policy. You can choose between the National Flood Insurance Program (NFIP) or a growing private market. Checking a property’s specific flood designation before making an offer is a proven methodology to ensure your investment remains protected against the unpredictable elements of a tropical climate.

The Four-Point Inspection Requirement

For homes older than 30 years, carriers require a Four-Point inspection. This report focuses on four critical systems: HVAC, electrical, plumbing, and the roof. A failed inspection in any of these areas can derail a mortgage approval and lead to unexpected hidden costs buying a home Florida residents face when they are forced to make immediate repairs. When you are ready to buy a property, having a guide who understands these technical requirements ensures you move forward with total clarity and zero surprises. We help you identify these red flags long before they become expensive liabilities.

Ongoing Ownership: The Costs That Start After Closing

The celebration of closing day often masks the reality of the first year’s carrying costs. While we’ve discussed the immediate transaction, the true weight of your investment settles in during the months that follow. Many buyers experience a sense of shock when their first full year of ownership reveals expenses the previous owner never had to pay. This is where a partnership oriented approach becomes vital. We want you to feel supported, empowered, and fully prepared for the long term. Understanding these hidden costs buying a home Florida residents face is the only way to build a sustainable, stress-free budget.

Florida’s climate and infrastructure create unique financial requirements that differ from almost any other state. From the way your lawn is watered to the way your community was built, every detail carries a price tag. We provide the steady hand you need to navigate these variables. Our goal is to replace your uncertainty with a sense of clarity. By looking at the data for 2026, we can project your expenses with professional confidence.

Property Tax Reassessment and the Homestead Exemption

Florida’s “Save Our Homes” cap is a shield for the seller, but it offers no protection to you. This law limits annual assessment increases to 3% for current owners. When you buy the home, that cap vanishes. The property is reassessed at its current market value, which often results in a tax bill significantly higher than what the seller paid. It’s a reset. To mitigate this, you must file for your Homestead Exemption by the March 1st deadline. In 2026, voters are even considering an increase to this exemption, potentially saving you more in 2027 and 2028. We recommend using a local tax estimator to project your 2027 bill accurately so you aren’t caught off guard by a “sticker shock” reassessment.

HOA vs. CDD: What is the Difference?

While an HOA manages your community’s lifestyle, a Community Development District (CDD) funds its very foundation. CDD fees are bond funded infrastructure costs for roads, utilities, and amenities. These are typically included in your annual tax bill and can range from $1,500 to $3,000 for single family homes. In contrast, HOA fees are paid monthly or quarterly and cover maintenance or security. It’s common for new developments to have both. We help you identify these recurring hidden costs buying a home Florida developers often place in the fine print of a listing. Knowing the difference ensures you aren’t paying twice for the same sense of security and community.

Finally, your maintenance budget must account for the tropical environment. Humidity, salt air, and relentless sun are the silent architects of your repair schedule. AC systems work harder here. Roofs face more intense UV exposure. Even your utility bill might include high “hidden” costs for irrigation if you aren’t using reclaimed water. A methodical, logical, and steady approach to your first year’s budget will ensure your Florida dream remains a source of joy rather than a source of strain.

New Construction & Specialty Considerations in Florida

A brand-new home offers a sense of security, modern efficiency, and a pristine start. However, the path to a new build is often paved with hidden costs buying a home Florida developers don’t always highlight in the model center. We are here to help you see past the granite countertops and open floor plans. Our goal is to ensure you understand the full financial scope of a new construction contract before you sign on the dotted line. It is about balance, protection, and advocacy.

One of the most frequent surprises is the “Working Capital Contribution.” This is a one-time fee, often equal to two or three months of HOA dues, collected at closing to fund the association’s initial operations. You might also encounter developer fees that cover the administrative costs of the community’s legal formation. These are separate from your down payment and the standard closing costs we discussed earlier. When you choose to sell new construction or purchase a fresh build, having a seasoned expert ensures these line items don’t catch you off guard.

The Builder’s Closing Cost Contribution

Builders often provide enticing incentives, such as thousands of dollars toward your closing costs. While these offers are attractive, they often require you to use the builder’s preferred lender or title company. This can lead to higher interest rates or less flexibility in your loan terms. We recommend maintaining independent representation to review these contracts. Even with a new build, you should invest in an independent “phase inspection” to verify the structural integrity at every stage. This is a proven methodology for long-term peace of mind.

Lot Premiums and Externalities

The base price of a home rarely includes the specific land it sits on. Lot premiums are a significant factor in Florida, where a water view, a preserve view, or even a simple corner lot can add between $10,000 and $100,000 to your final price. Beyond the lot, you must budget for the “missing” essentials. Builders often leave out window treatments, gutters, and screened-in lanais. These are not just luxuries; in our climate, they are practical necessities for comfort and home protection. A methodical approach to these extras ensures your final budget is as solid as your new foundation. We help you identify these hidden costs buying a home Florida developers often leave in the fine print.

Strategic Budgeting: Navigating the Market with a Specialist

Professional representation serves as your primary defense against the hidden costs buying a home Florida often presents. It isn’t just about finding a house; it’s about securing a future. We act as your steady hand, ensuring every financial detail is scrutinized before you commit. By identifying red flags in the 2026 insurance and tax landscape early, we move you from a place of uncertainty to a position of professional confidence. You deserve a process that feels transparent, stable, and entirely under your control.

Negotiation is your most powerful tool for cost reduction. While many buyers assume transaction fees are fixed, a specialist knows how to shift these burdens back to the seller. Whether it’s asking for a credit to cover the 0.2% intangible tax or negotiating a lower price to offset a high CDD fee, these movements create immediate value. Our partnership-oriented approach focuses on your long-term success. We look beyond the initial acquisition to effective property management and value growth, replacing stress with a clear sense of security.

The Advocate Advantage

A specialist provides a level of scrutiny that goes far beyond a simple walkthrough. We review the Closing Disclosure and HUD-1 documents with a methodical eye, catching the clerical errors or duplicate fees that can inflate your final bill. Think of us as a mentor who identifies “money pit” properties before they drain your reserves. Local expertise is the best insurance you can have against the hidden costs buying a home Florida shoppers frequently encounter. It turns a volatile marketplace into a structured path toward your goals.

Your Next Steps to a Secure Purchase

The 90 days leading up to your closing are critical for financial stability. You should finalize your 2026 insurance quotes, use a local tax estimator for your 2027 bill, and verify any community-specific assessments. We’re here to guide you through this checklist with ease. If you’re ready to move forward with total clarity, Contact The Florida Real Estate Specialist for a reassuring path home. We provide the calm in the storm, ensuring your transition is both secure and successful.

Secure Your Florida Future with Total Confidence

You now have a clear view of the 2026 landscape. We’ve navigated the complexities of tax resets, insurance mitigation, and the unique fee structures of new construction. These details are the foundation of a successful purchase. Understanding the hidden costs buying a home Florida involves allows you to move from a position of anxiety to one of professional ease. It’s about clarity, security, and preparedness.

Expert representation for new construction and a comprehensive property management perspective ensure your investment is protected long after you receive the keys. We provide seasoned guidance in the Florida residential market to act as your steady hand. Are you ready to replace uncertainty with a proven methodology? Download Our 2026 Florida Buyer’s Budgeting Worksheet to begin your journey with a precise, line-item plan. Your dream home is within reach, and we’re here to ensure you arrive there with zero surprises and total peace of mind. Welcome home.

Frequently Asked Questions

What are the average closing costs for a home in Florida?

Average closing costs typically range between 2% and 5% of the total purchase price. This includes essential items such as title insurance, documentary stamp taxes, and loan origination fees. While these figures vary by county and lender, budgeting on the higher end provides a sense of security. We help you scrutinize these line items to ensure your transaction is both transparent and fair.

Do I really need flood insurance if I am not on the coast?

Flood insurance is a wise investment even for homes located far from the coastline. Standard homeowners policies don’t cover damage from rising groundwater or heavy tropical rainfall. Florida’s unique geography means that many areas are susceptible to flooding regardless of their proximity to the beach. Securing a separate policy provides an essential layer of protection and peace of mind for your investment.

What is a CDD fee, and is it permanent?

A Community Development District (CDD) fee is a bond funded charge used to build and maintain community infrastructure like roads and utilities. While the bond portion may eventually be paid off, the operations and maintenance part usually remains. These fees are typically collected through your annual property tax bill. Understanding this distinction is vital for accurate long-term budgeting in newer master-planned communities.

Why are property taxes in Florida so confusing for new buyers?

Property taxes are often the most misunderstood aspect of the market. Because of the Save Our Homes cap, the seller’s current bill is likely much lower than what yours will be. Your taxes are based on the new assessed value after the sale. This reset is one of the most significant hidden costs buying a home Florida residents face. We provide the clarity you need to project these costs with total confidence.

How much should I budget for home maintenance in Florida?

Budgeting 1% to 2% of your home’s value for annual maintenance is a proven methodology for Florida homeowners. The relentless sun and high humidity levels place significant stress on your roof and HVAC systems. Regular servicing prevents minor issues from becoming major financial burdens. A methodical approach to upkeep ensures your home remains a stable asset and a comfortable sanctuary for years to come.

Can a real estate agent help me reduce my closing costs?

A dedicated specialist advocates for your interests by negotiating seller concessions and credits. We can often shift a portion of the closing costs back to the seller, reducing your cash-to-close requirement. By reviewing your Closing Disclosure with a professional eye, we identify potential errors or duplicate charges. This advocacy replaces uncertainty with a sense of ease, ensuring you receive the best possible terms.

Is it more expensive to buy new construction in Florida?

New construction often carries unique expenses like working capital contributions and lot premiums. The base price you see in a model home rarely includes the personalization upgrades or essential landscaping you’ll want. These are common hidden costs buying a home Florida developers may not emphasize initially. Our seasoned guidance helps you account for every detail, ensuring your new build remains a source of joy rather than strain.

What happens to the property taxes after the first year of ownership?

After your first year, your property taxes will reflect the new assessed value based on your purchase price. If you’ve filed for your Homestead Exemption, your future assessment increases will be capped at 3% annually. This cap provides a foundation of stability for your long-term housing costs. We ensure you meet all critical deadlines so you can enjoy the full benefits of Florida’s tax protections.