Miami's luxury real estate market is experiencing an unprecedented transformation in 2026, with over 15,000 new condos delivering across Brickell, Edgewater, Miami Beach, and Coconut Grove. But navigating this golden opportunity requires more than just deep pockets—it demands strategic thinking, meticulous due diligence, and insider knowledge that separates savvy buyers from those who overpay or inherit costly surprises.

📊 Four-year high in South Florida – $10 Million+ Sales

Whether you're an international investor, a California executive relocating for tax advantages, or a lifestyle buyer seeking your dream waterfront residence, this comprehensive guide delivers the practical strategies you need to secure the best new construction luxury homes Miami has to offer—at the right price, with the right terms, and with full protection of your investment.

Table of Contents

- Step 1: Master the Pre-Construction Buying Timeline

- Step 2: Decode Developer Reputation Like a Wall Street Analyst

- Step 3: Strategic Neighborhood Selection Beyond the Obvious

- Step 4: Negotiate Deposit Structures That Protect Your Capital

- Step 5: Navigate Financing in Miami's New Construction Market

- Step 6: The HOA and Reserve Audit No One Tells You About

- Step 7: Secure Customization Rights and Design Upgrades

- Step 8: Assignment Clauses and Exit Strategy Planning

- Step 9: The Final Walkthrough and Closing Checklist

Step 1: Master the Pre-Construction Buying Timeline

Understanding the multi-phase sequence of pre-construction purchases separates sophisticated buyers from those caught off-guard by developer timelines and deposit schedules.

The Reservation Phase: Securing Your Position

The journey typically begins with a reservation agreement—a generally non-binding position in line paired with a refundable deposit ranging from $25,000 to $100,000 depending on the project's luxury tier. This is not your full legal commitment; it's strategic positioning.

Pro Strategy: Treat reservation as your negotiation window. Before signing the purchase contract, confirm:

- Unit change flexibility if better inventory becomes available

- Assignment rights for future resale flexibility

- Refund conditions and exact timelines

- Upgrade selection deadlines and customization windows

"Pre-construction timelines typically span 24-48 months from contract to delivery"

— Multiple Miami luxury developments(https://limova-public-v2.s3.eu-central-1.amazonaws.com/blog-images/blog-image-1774184674137-dbl0d21e.jpeg)

{kind=link}

Construction Milestones and Payment Triggers

Typical deposit structure for Miami luxury new construction:

- Reservation: $25K-$100K (refundable until contract)

- Contract execution: 10-20% of purchase price

- Groundbreaking: Additional 5-10%

- Foundation completion: Additional 5-10%

- Structural topping off: Additional 5-10%

- Balance at closing: Remaining 70-80%

Insider Tip: Request that all deposits be held in an interest-bearing escrow account with a reputable title company. In some agreements, you may negotiate to receive the interest earned on your deposits—a detail that can amount to thousands of dollars over a 24-36 month construction period.

Step 2: Decode Developer Reputation Like a Wall Street Analyst

In Miami's booming market, developer selection is your single most important risk mitigation strategy. The difference between a seamless delivery and a construction nightmare often comes down to track record.

The Developer Due Diligence Checklist

Before committing a deposit, conduct this forensic analysis:

1. Completed Project History

- How many luxury projects has the developer delivered in Miami?

- What was the average delay between promised and actual delivery dates?

- Review online buyer forums and condo association meeting minutes from completed buildings

2. Financial Strength Indicators

- Is the construction loan already secured? (50-70% presale requirement is common)

- Who is the lender? (Major institutions signal stronger underwriting)

- What percentage of units are already pre-sold?

3. Design and Construction Team

- Architect reputation (Arquitectonica, Adrian Smith + Gordon Gill, Foster + Partners are gold standard)

- General contractor track record

- Interior designer portfolio for branded residences

4. Legal and Regulatory Standing

- Search for lawsuits against the developer in Miami-Dade court records

- Verify all permits and zoning approvals are in place

- Confirm compliance with Florida's milestone inspection requirements

📊 Foreign buyers in Miami – 52% of new-construction purchases

Red Flags That Should Stop You Cold

- First-time developer in the luxury segment without established partners

- Vague completion timelines or unwillingness to commit to delivery windows

- Excessive presale incentives (suggests difficulty moving inventory)

- No construction loan secured 12+ months after sales launch

- Negative reviews from buyers in previous projects regarding quality or delays

Case Study: In 2026, projects like Una Residences Brickell (OKO Group and Cain International) and NoMad Residences Wynwood (Related Group) demonstrate the gold standard—established developers with multiple successful Miami deliveries, secured financing, and on-time or early completion.

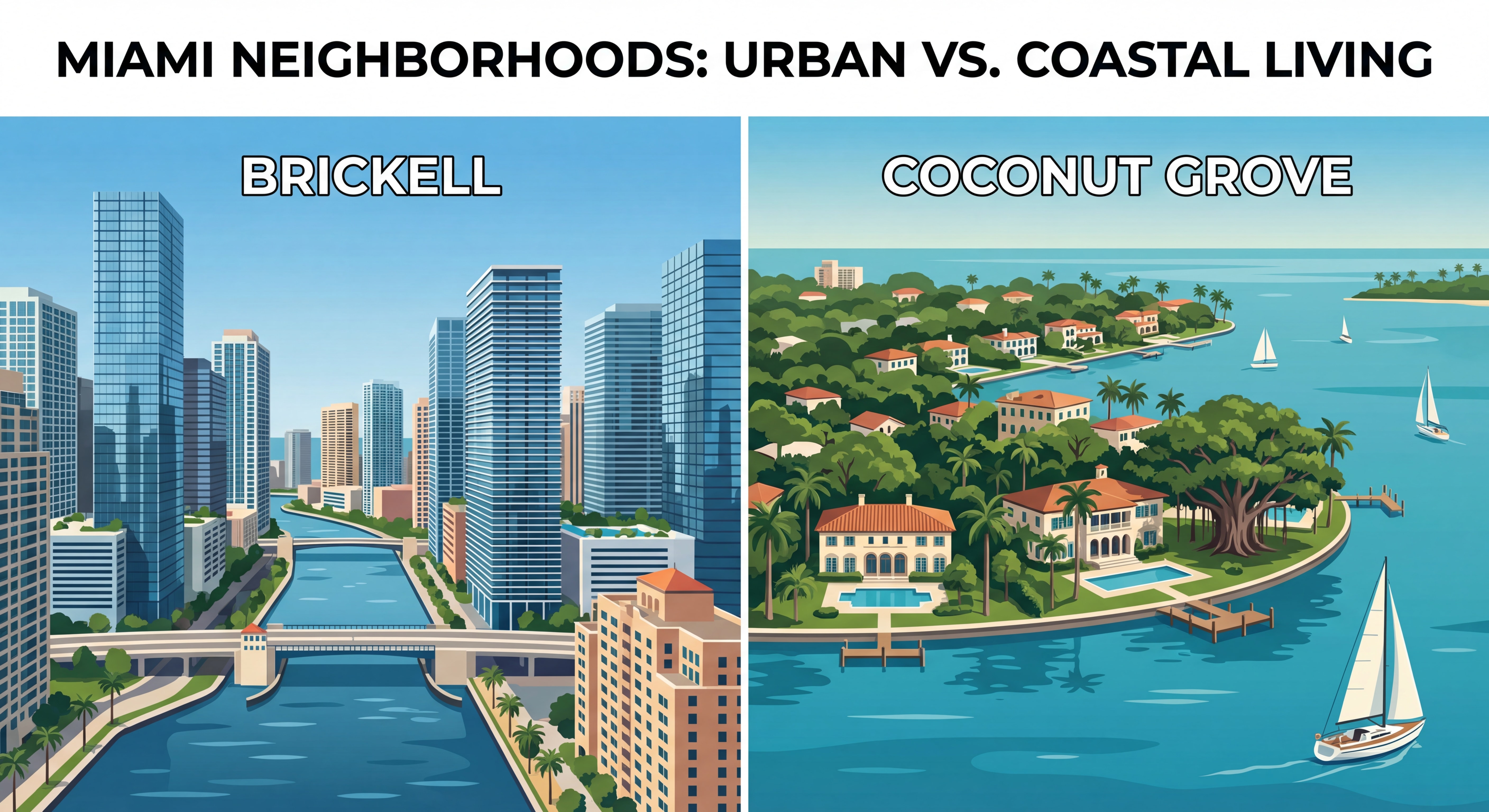

Step 3: Strategic Neighborhood Selection Beyond the Obvious

Miami luxury real estate in 2026 offers distinct value propositions across neighborhoods. Understanding the nuanced differences helps you align investment goals with location strategy.

Brickell: Urban Sophistication and Rental Income Powerhouse

Price Range: $850-$2,000+ per square foot

Median Luxury Condo: $1.5M-$1.6M

HOA Fees: $700-$2,500/month

Best For:

- Investors seeking short-term rental income (many buildings allow Airbnb)

- Young professionals and corporate relocators

- Buyers prioritizing walkability and urban amenities

Strategic Considerations:

- Latin American buyers dominate new Brickell inventory for rental conversion

- Proximity to financial district supports strong rental demand

- New branded residences (St. Regis, Cipriani, Dolce & Gabbana) command premium pricing

Insider Tip: Focus on buildings with clear short-term rental policies in the condo documents. Florida's new reserve requirements mean you should verify the building's structural integrity reserve study (SIRS) is fully funded to avoid special assessments.

Edgewater: Waterfront Value with Appreciation Upside

Price Range: $650-$1,103 per square foot

Median Asking: $710,000

HOA Fees: $1,110-$2,500/month (bayfront towers)

Best For:

- Buyers seeking waterfront views without Miami Beach premiums

- Investors targeting 7-8% gross rental yields

- Those wanting proximity to Design District and Wynwood culture

Market Dynamics:

- 287 active listings as of March 2026 (high inventory = negotiation leverage)

- Average 234 days on market (compared to 118 in Q4 2025)

- Rental rates averaging $6,763/month

Strategy: Edgewater's higher inventory levels in 2026 create buyer leverage. Negotiate harder on pricing, request seller-paid closing costs, and explore developer incentives like upgraded appliance packages or furniture credits.

Miami Beach: Trophy Assets and International Prestige

Price Range: $1,200-$3,000+ per square foot

Target Buyer: Ultra-high-net-worth seeking primary residence or pied-à-terre

Best For:

- Lifestyle buyers prioritizing oceanfront living and resort amenities

- International buyers seeking recognizable luxury addresses

- Those valuing privacy and full-service branded experiences

Flagship Projects: The Ritz-Carlton Residences Miami Beach, Rosewood Residences (at the Raleigh), and Shore Club Private Residences exemplify the tier.

Coconut Grove: Boutique Luxury and Family-Oriented Living

Price Range: $1,000-$2,500+ per square foot

HOA Fees: $1,500/month average (boutique buildings)

Best For:

- Families seeking top schools and green spaces

- Buyers wanting village atmosphere with luxury finishes

- Those prioritizing privacy over high-rise density

2026 Spotlight: The Well Coconut Grove (194 residences, 50% presold, $410M construction loan secured) and Four Seasons Private Residences Coconut Grove represent the neighborhood's evolution toward wellness-focused luxury.

Comparative Analysis: Where to Invest Based on Goals

| Goal | Best Neighborhood | Key Advantage |

|---|---|---|

| Maximum rental income | Brickell | Short-term rental flexibility, corporate demand |

| Appreciation potential | Edgewater | Current buyer's market, waterfront upside |

| Trophy asset/prestige | Miami Beach | International recognition, oceanfront scarcity |

| Family primary residence | Coconut Grove | Schools, parks, boutique luxury |

| Tax efficiency + lifestyle | Any (no state income tax) | Florida tax advantages across all areas |

Step 4: Negotiate Deposit Structures That Protect Your Capital

Pre-construction deposits represent significant capital tied up for 24-48 months. Strategic structuring protects your liquidity and maximizes flexibility.

Standard vs. Optimized Deposit Schedules

Developer's Preferred Structure:

- 10% at contract signing

- 10% at groundbreaking (6-12 months later)

- 10% at topping off (18-24 months later)

- 70% at closing

Sophisticated Buyer's Negotiated Structure:

- 5% at contract signing

- 5% at foundation completion (8-14 months later)

- 5% at topping off (20-26 months later)

- 5% at certificate of occupancy

- 80% at closing

Why This Matters: Extending deposit timelines and reducing early percentages preserves your investment capital for other opportunities while construction progresses.

Escrow Protection Strategies

Non-negotiable requirements:

- Independent escrow agent (title company or law firm, not developer-controlled account)

- Written escrow instructions specifying release conditions

- Interest-bearing account with clear documentation of who receives interest

- Refund timeline if financing contingency is triggered (30-45 days maximum)

Advanced Strategy: For purchases above $3 million, negotiate a letter of credit option in lieu of some cash deposits. This keeps your capital working while still satisfying the developer's presale requirements.

Assignment Rights: Your Hidden Exit Strategy

Assignment clauses allow you to sell your contract to another buyer before closing—a critical flexibility tool if circumstances change.

Typical Developer Restrictions:

- Outright prohibition on assignments

- Assignment allowed only after 50% of deposits paid

- Developer approval required (with subjective criteria)

- Assignment fees of 2-5% of purchase price

What to Negotiate:

- Approval process with objective criteria (financial qualification only)

- Reduced assignment fees (1-2% vs. 5%)

- Earlier assignment rights (after 30% deposits vs. 50%)

- No developer right of first refusal at your assignment price

Real-World Application: In Miami's 2026 market with rising inventory, assignment rights provide an exit if you need liquidity before delivery or if market conditions shift unfavorably.

Step 5: Navigate Financing in Miami's New Construction Market

While many luxury buyers pay cash (especially international purchasers), strategic financing can enhance returns and preserve capital for diversification.

Pre-Construction Financing Challenges

Why Banks Are Cautious:

- No completed building to appraise

- 24-48 month timeline creates rate uncertainty

- Florida's new condo regulations add underwriting complexity

- Structural reserve requirements impact building financials

The Three-Phase Financing Strategy

Phase 1: Pre-Qualification (Before Contract)

- Secure pre-approval from lenders experienced with Miami new construction

- Understand loan-to-value limits (typically 70-75% for luxury condos)

- Verify the building is on the lender's approved list

Phase 2: Rate Lock Strategy (12 Months Before Delivery)

- Monitor delivery timeline announcements from developer

- Explore bridge loan options if you need to close before permanent financing is ready

- Consider adjustable-rate mortgages (ARMs) if you plan to refinance or sell within 5 years

Phase 3: Final Underwriting (60-90 Days Before Closing)

- Lender will require completed building appraisal

- HOA budget and reserve study review

- Final condo document approval (warrantability)

📊 Miami-Dade condo sales Q1 2026 – 14% year-over-year increase

Bridge Loans: The Sophisticated Buyer's Tool

Miami's 2026 delivery wave has increased demand for condo bridge loans—short-term financing that allows you to close quickly when the developer issues the closing notice, then refinance into permanent financing on your timeline.

When Bridge Loans Make Sense:

- You need to close within developer's 30-60 day window

- You're selling another property but timing doesn't align perfectly

- You want to lock in pre-construction pricing but preserve permanent financing flexibility

- You're an international buyer establishing U.S. credit history

Typical Terms:

- 12-24 month duration

- 65-75% loan-to-value

- Interest-only payments

- Rates 2-4% above conventional mortgages

Cash vs. Financing: The Strategic Analysis

| Scenario | Recommendation | Rationale |

|---|---|---|

| Purchase under $1M | Consider financing | Preserve capital, mortgage interest deduction |

| Purchase $1M-$3M | Hybrid (50% down) | Balance leverage with favorable terms |

| Purchase $3M+ | Cash if liquid | Avoid appraisal challenges, faster closing |

| International buyer | Cash or private banking | U.S. mortgage qualification complexity |

| Investment property | Finance if possible | Leverage enhances ROI on appreciation |

Step 6: The HOA and Reserve Audit No One Tells You About

Florida's post-Surfside condo safety legislation has fundamentally changed the financial landscape for high-rise buildings. Understanding these requirements protects you from devastating special assessments.

The New Florida Condo Reality (HB 913 and Beyond)

Mandatory Requirements Effective 2026:

- Structural Integrity Reserve Studies (SIRS) for buildings 3+ stories

- Full reserve funding starting January 1, 2026 (no more waiving reserves)

- Milestone inspections at 30 years and every 10 years thereafter

- Transparent financial reporting on association websites

What This Means for Buyers: Buildings with underfunded reserves or deferred maintenance will face massive special assessments in 2026-2027 as they scramble to comply.

Your Pre-Purchase Reserve Audit Checklist

Documents to Request and Review:

-

Most Recent Reserve Study

- When was it completed? (Should be within 12 months)

- What is the current funding percentage? (Target: 70%+ funded)

- What major components need replacement in next 5 years?

-

HOA Budget Breakdown

- What percentage goes to reserves vs. operating expenses?

- Has insurance increased significantly year-over-year?

- Are there any pending or approved special assessments?

-

Milestone Inspection Reports

- For buildings 30+ years old, review structural integrity findings

- Identify any "substantial structural deterioration" flags

- Verify remediation plans and funding sources

Red Flag Calculator:

Average Miami-Dade luxury high-rise HOA fees: $1,900/month (2026)

Insurance component: $377/month (up 25% year-over-year)

Warning signs:

- HOA fees below $1,200/month for full-service waterfront building (likely underfunded)

- Reserves funded below 50% (special assessment risk)

- Insurance costs increasing 30%+ annually (building risk profile issues)

- Pending litigation against the association

The Questions Sophisticated Buyers Ask

Before signing a contract, demand answers to:

- "What is the current reserve funding percentage, and what is the target?"

- "Have there been any special assessments in the past 5 years? What were they for?"

- "What major capital expenditures are planned in the next 3-5 years?"

- "Is the building in compliance with all milestone inspection requirements?"

- "What is the association's insurance deductible, and do unit owners need supplemental coverage?"

Insider Strategy: For new construction, verify the developer's initial reserve funding commitment. Many developers seed the reserve account with 10-15% of the first year's budget, but some provide minimal funding, setting up immediate shortfalls.

Step 7: Secure Customization Rights and Design Upgrades

New construction's greatest advantage is the ability to customize finishes and layouts to your exact specifications—but only if you negotiate these rights and understand the timelines.

The Design Selection Timeline

Typical Developer Schedule:

- 6-12 months before delivery: First design center appointment

- 4-8 months before delivery: Final selections deadline

- 2-4 months before delivery: No changes allowed (construction locked)

Pro Strategy: Negotiate earlier access to design selections in your purchase contract—especially for units on higher floors that will be completed later. This gives you more time to make thoughtful decisions and potentially secure upgraded options before they're allocated.

What You Can (and Can't) Customize

Typically Customizable:

- Flooring materials (hardwood, marble, porcelain)

- Kitchen and bathroom countertops and backsplashes

- Cabinet finishes and hardware

- Lighting fixtures and smart home technology packages

- Paint colors and accent walls

- Appliance upgrades (within approved brand parameters)

Typically Non-Customizable:

- Structural elements and load-bearing walls

- Plumbing and electrical rough-in locations

- Window and balcony door specifications

- HVAC system type and capacity

- Building-wide smart home infrastructure

Upgrade Budget Strategy

Developer Pricing vs. After-Delivery:

| Upgrade Category | Developer Price Premium | Post-Delivery Cost | Strategic Choice |

|---|---|---|---|

| Flooring | 20-30% markup | Same or lower | Wait for post-delivery |

| Kitchen appliances | 15-25% markup | 10-20% higher retail | Upgrade with developer |

| Smart home tech | 30-40% markup | 20-30% higher | Negotiate package discount |

| Lighting fixtures | 40-50% markup | Same or lower | Wait for post-delivery |

| Countertops | 25-35% markup | 30-40% higher | Upgrade with developer |

The $50,000 Rule: For most luxury buyers, allocating approximately $50,000-$100,000 to strategic developer upgrades (appliances, countertops, smart home) while deferring cosmetic items (lighting, paint, some flooring) to post-delivery optimizes value.

Negotiating Upgrade Credits

Leverage Points for Free Upgrades:

- Early contract signing (first 20% of units sold)

- All-cash purchase (no financing contingencies)

- Purchasing multiple units (investor bulk discount)

- Slow sales period (increased inventory, developer motivation)

Sample Negotiation Script:

"I'm prepared to sign this week with 10% deposit, but I'd like you to include the upgraded Gaggenau appliance package and marble flooring in the main living areas as part of the base price. Can we make that work?"

Success Rate: In Miami's current buyer's market (Q1 2026), developers are offering $25,000-$75,000 in upgrade credits or furniture packages to secure contracts, especially in buildings below 50% presold.

Step 8: Assignment Clauses and Exit Strategy Planning

Even if you intend to occupy your new luxury condo, market conditions can change over a 24-36 month construction period. Building in exit flexibility protects your investment.

Understanding Assignment Mechanics

What is Assignment?

Selling your purchase contract (and associated rights/obligations) to a new buyer before the building is completed and you take title.

Why Developers Restrict It:

- Loss of control over buyer financial qualification

- Potential to undermine new sales if assignors discount heavily

- Administrative burden of contract transfers

Why Buyers Need It:

- Job relocation or life circumstances change

- Market appreciation creates profitable exit opportunity

- Liquidity needs arise during construction period

The Assignment Negotiation Framework

Developer's Starting Position:

- No assignments allowed, or

- Assignment only after 75% of deposits paid

- Developer approval required (subjective)

- Assignment fee of 5-10% of purchase price

- Developer right of first refusal at assignment price

Sophisticated Buyer's Target:

- Assignment allowed after 50% of deposits paid

- Approval based solely on buyer financial qualification (objective criteria)

- Assignment fee of 1-2% of purchase price (to cover administrative costs)

- No developer right of first refusal

- Clear 30-day approval timeline

Compromise Position:

Assignment allowed after 60% deposits paid, 2% assignment fee, developer approval not to be unreasonably withheld, 45-day approval process.

Tax Implications of Assignment

Critical Consideration: Assignment sales are typically treated as ordinary income (not capital gains) because you're selling a contract right, not real property.

Example:

- Purchase price: $2,000,000

- Deposits paid: $600,000 (30%)

- Assignment price: $2,400,000

- Gross profit: $400,000

- Tax treatment: Ordinary income (up to 37% federal + state)

vs. Holding to Closing:

- Same appreciation: $400,000

- Tax treatment: Long-term capital gains (20% federal if held 1+ year after closing)

Strategy: If you anticipate selling during construction, consult a tax advisor about structuring the purchase through an LLC or other entity that may provide more favorable treatment.

Step 9: The Final Walkthrough and Closing Checklist

The weeks before closing are when sophisticated buyers protect their investment through meticulous inspection and verification.

The 60-Day Pre-Closing Sprint

Timeline and Action Items:

60 Days Out:

- Receive closing notice from developer

- Confirm exact closing date and balance due

- Finalize financing (if applicable) and order appraisal

- Schedule final walkthrough (typically 7-10 days before closing)

45 Days Out:

- Review and approve final condo documents (declaration, bylaws, rules)

- Verify HOA budget and reserve funding levels

- Confirm certificate of occupancy has been issued

- Review title commitment and survey

30 Days Out:

- Wire deposit for closing funds to escrow (verify wire instructions by phone)

- Purchase homeowners insurance (required even with HOA master policy)

- Arrange for utilities and internet setup

- Review closing disclosure and settlement statement

7-10 Days Out:

- Conduct final walkthrough with punch-list checklist

- Photograph any defects or incomplete items

- Verify all contracted upgrades and finishes were installed

- Test all appliances, plumbing fixtures, and smart home systems

The Final Walkthrough Punch List

Bring These Tools:

- Smartphone camera for documentation

- Tape measure for verification of square footage

- Level for checking floor and counter installation

- Outlet tester for electrical systems

- Flashlight for inspecting closets and mechanical areas

Systematic Inspection Checklist:

Structural and Finishes:

- Floors level and free of damage

- Walls and ceilings smooth, no cracks or water stains

- Windows and doors operate smoothly, no gaps

- Balcony waterproofing and drainage functioning

- All agreed-upon finishes and upgrades installed

Kitchen:

- All appliances installed and operational

- Countertops level, no chips or cracks

- Cabinet doors and drawers align and close properly

- Plumbing fixtures don't leak (run water for 5+ minutes)

- Garbage disposal and dishwasher functioning

Bathrooms:

- Shower/tub water pressure adequate

- No leaks in plumbing fixtures

- Proper drainage (no standing water)

- Ventilation fan operational

- Countertops and tile grouting complete

Systems:

- HVAC heating and cooling both functional

- Smart home systems programmed and operational

- All electrical outlets and switches working

- Internet/cable rough-ins in correct locations

- Security system (if applicable) functioning

Common Areas (if applicable to your unit):

- Private elevator (if contracted) operational

- Storage unit assigned and accessible

- Parking space(s) marked and available

Handling Punch-List Items

Developer's Obligation: Most contracts require the developer to deliver the unit in "substantial completion" with only minor punch-list items remaining.

Your Leverage Strategy:

- Document everything during walkthrough with photos and written list

- Require written commitment from developer on completion timeline for each item

- Consider escrow holdback for significant incomplete items (negotiate 150% of estimated repair cost held in escrow until completion)

- Don't accept vague promises—get specific dates and contractor names

Red Flag Items That Should Delay Closing:

- Non-functional HVAC, plumbing, or electrical systems

- Significant water damage or active leaks

- Missing contracted upgrades or finishes

- Structural defects or safety hazards

- Certificate of occupancy not yet issued

Questions Fréquentes (FAQ)

What is the typical deposit structure for Miami luxury new construction condos?

Most developers require staged deposits totaling 20-30% of the purchase price over the construction period: typically 10% at contract signing, 10% at groundbreaking or foundation completion, and 10% at structural topping off, with the remaining 70-80% due at closing. Sophisticated buyers often negotiate extended timelines and lower early percentages to preserve capital.

How do I verify a developer's reputation before committing to a pre-construction purchase?

Conduct forensic due diligence including: reviewing the developer's completed project history in Miami, analyzing delivery timelines versus promises, verifying construction loan approval and presale percentages, researching the architect and design team credentials, searching Miami-Dade court records for litigation, and reading buyer reviews from previous developments. Established developers like Related Group, OKO Group, and Terra demonstrate the gold standard.

Should I pay cash or finance a luxury new construction condo in Miami?

The decision depends on your liquidity, investment strategy, and purchase price. For properties under $1M, financing preserves capital and provides tax deductions. For $1M-$3M, a hybrid approach (50% down) balances leverage with favorable terms. For $3M+ purchases, cash often makes sense to avoid appraisal challenges and expedite closing. International buyers typically pay cash due to U.S. mortgage qualification complexity.

What are Florida's new condo reserve requirements and how do they affect my purchase?

Florida's HB 913 legislation requires structural integrity reserve studies (SIRS) for buildings 3+ stories, mandatory full reserve funding starting January 1, 2026, and milestone structural inspections at 30 years and every 10 years thereafter. Buyers must verify that new construction developers adequately fund initial reserves and that the HOA budget includes proper reserve allocations to avoid future special assessments that can reach tens of thousands of dollars per unit.

Can I customize finishes in a new construction luxury condo, and when do I need to decide?

Most developers allow customization of flooring, countertops, cabinetry, appliances, lighting, and paint within approved parameters. Design center appointments typically occur 6-12 months before delivery, with final selections due 4-8 months before completion. Strategic buyers upgrade items that cost more post-delivery (appliances, countertops) while deferring cosmetic elements (lighting, paint) that can be changed later at lower cost.

What is an assignment clause and why should I negotiate for it?

An assignment clause allows you to sell your purchase contract to another buyer before closing—providing exit flexibility if circumstances change during the 24-48 month construction period. Developers often restrict assignments, but sophisticated buyers negotiate for assignment rights after 50-60% of deposits are paid, with objective approval criteria, reasonable fees (1-2%), and clear timelines. This protects against job relocation, market shifts, or liquidity needs.

How much should I budget for HOA fees in Miami luxury new construction?

Miami-Dade luxury high-rise HOA fees averaged $1,900/month in 2026, with insurance comprising approximately $377/month. Brickell buildings typically range $700-$2,500/month depending on amenities, while Edgewater bayfront towers run $1,110-$2,500/month. Coconut Grove boutique buildings average $1,500/month. Always verify what's included (insurance, reserves, amenities, staffing) and review the reserve funding percentage to assess special assessment risk.

Chiffres Clés

📊 174% above national average—Miami luxury real estate prices in 2026 (Source: HousingWire)

💰 $10 Million+ luxury home sales hit four-year high in South Florida (Source: Realtor.com)

🌍 52% of new-construction purchases by foreign buyers in Miami (Source: New York Post)

🏗️ 15,000+ luxury condos delivering in Miami through 2026 (Source: Multiple industry sources)

Your Next Steps: Execute With Confidence

Miami's new construction luxury market in 2026 presents extraordinary opportunities for buyers who approach the process with strategy, diligence, and expert guidance. The difference between a profitable investment and a costly mistake often comes down to the details covered in this guide—from deposit structure negotiation to reserve study analysis to assignment rights protection.

Your Action Plan:

- Identify your top 2-3 neighborhoods based on investment goals and lifestyle priorities

- Research developers with proven track records in your target areas

- Assemble your advisory team: experienced buyer's agent, Florida real estate attorney, and mortgage specialist (if financing)

- Visit sales galleries armed with the negotiation frameworks from this guide

- Conduct thorough due diligence on developers, buildings, and financial structures before signing contracts

The Miami luxury new construction market rewards those who combine vision with meticulous execution. Whether you're securing a Brickell pied-à-terre with Biscayne Bay views, a Miami Beach oceanfront sanctuary, or a Coconut Grove family estate, the strategies in this playbook position you to navigate the process like a seasoned pro—protecting your capital, maximizing value, and ultimately securing the luxury Miami home of your dreams.

Ready to begin your Miami luxury real estate journey? The market is moving quickly, but with the right preparation and expert guidance, you can move faster and smarter than the competition.